Paul Ryan is an epic failure

Let’s briefly take stock of Speaker Paul Ryan’s career.

Let’s briefly take stock of Speaker Paul Ryan’s career.

Elected to Congress in 1998, Ryan spent most of his first decade as a backbencher. His most ambitious proposal in those early years was a plan to privatize Social Security that even the Bush White House labeled as “irresponsible.”

Then he became the highest-ranking Republican on the House Budget Committee and, later, a committee chair. In these roles, Ryan revealed his two great talents — convincing his fellow Republicans to vote for laissez-faire proposals that had no chance of becoming law, and convincing Beltway pundits and reporters that he was some kind of policy wonk.

By the time Ryan’s reputation as the conservative movement’s Great Wonk convinced presidential candidate Mitt Romney to choose Ryan as his running mate, Ryan was the primary sponsor of just two bills that actually became law. One was a 2000 bill renaming a post office in his home town. The other was a 2004 bill modifying the excise tax on arrows. The kind Katniss Everdeen uses.

So the Speaker of the House has barely any experience in real governance. He’s never ushered a major policy proposal from conception to enactment. He’s never engaged in the kind of high-stakes coalition building where everyone at the table knows that their ideas have a real chance of becoming law. He’s distinguished himself primarily by his ability to take pot shots at President Obama and to pass bills that couldn’t survive a Senate filibuster.

And boy, does it show.

It’s tough to imagine a bigger put-up-or-shut-up moment in U.S. politics than Republican lawmakers’ current effort to roll back the Affordable Care Act. Since its passage, Republicans have attacked Obamacare with falsehoods about death spirals and with falsehoods about death panels — construing stopping Obamacare as literally a matter of life and death.

On the day the House passed the bulk of the Affordable Care Act, then-Minority Leader John Boehner spoke of the legislation in apocalyptic terms. “Today we stand here amidst the wreckage of what was once the respect and honor that this House was held in my our fellow citizens,” Boehner told his fellow lawmakers. “And we all know why it is so.”

After years to work on an Obamacare replacement, Ryan came up with a morass of austerity, unintentionally backwards ideas, and proposals to sacrifice America’s elders to their grandchildren.

Now, the Republican Party’s current leader predicts an apocalypse of a different kind if Obamacare remains law. Donald Trump has warned that House Republicans will face a “bloodbath” in the 2018 elections if they can’t get their act together in their Obamacare repeal effort.

Republicans had seven years to come up with a plan to repeal and replace the Affordable Care Act. They’ve promised over and over again to do so. There is no policy idea more essential to the GOP’s brand.

And yet Paul Ryan managed to mess this one up.

Paul Ryan’s Obamacare replacement mess

Ryan’s very first foray into the world of real policy design is an absolute mess. After having years to work on an Obamacare replacement, Ryan came up with a morass of austerity, unintentionally backwards ideas, and proposals to sacrifice America’s elders to their grandchildren.

According to the Congressional Budget Office (CBO), 24 million people will lose health coverage if Paul Ryan’s answer to the GOP’s pressing need to get rid of Obamacare, called the American Health Care Act, becomes law.

As Rachel Maddow notes, that’s roughly the population of Vermont, Alabama, North Dakota, South Dakota, Delaware, Montana, Rhode Island, Maine, New Hampshire, Idaho, West Virginia, Nebraska, New Mexico, Kansas, and Wyoming put together. There are 179 nations with less than 24 million residents. Passing the American Health Care Act is roughly the same thing as taking health care away from every single person in Australia.

And 24 million is also a conservative estimate. The Trump White House’s own internal analysis predicts that 26 million will lose coverage if Paul Ryan’s bill becomes law. That’s more than the population of Finland, Ireland, Norway, Singapore, and the Republic of the Congo put together.

Some of these consequences appear to be by design. The CBO predicts that Ryan’s bill would reduce Medicaid spending by $880 billion over ten years. It doesn’t take an economist to figure out what that’s going to do to people on Medicaid, and these cuts account for the bulk of the people who would become uninsured under Ryan’s bill — fourteen million people.

But many of the consequences of this bill appear to be due to poor design and not intentional efforts to kick people off their health insurance. One provision, for example, imposes a 30 percent surcharge on people who have a lapse in coverage for more than 63 days within a given year — so a health plan with a $300 monthly premium would instead cost $390.

The purpose of this provision is to encourage healthy people to remain insured by imposing a financial consequence if their coverage lapses. But CBO predicts that the surcharge will have the opposite effect. Although “roughly 1 million people would be induced to purchase insurance in 2018 to avoid possibly having to pay the surcharge in the future,” in most subsequent years “roughly 2 million fewer people would purchase insurance because they would either have to pay the surcharge or provide documentation about previous health insurance coverage.”

Moreover, the “people deterred from purchasing coverage would tend to be healthier than those who would not be deterred and would be willing to pay the surcharge.” So a mechanism Ryan intended to bring healthy people into insurance pools will instead chase them out.

Similarly, Ryan bragged shortly after the CBO report became public that his bill would “lower premiums,” and CBO did indeed predict that, after an initial spike in insurance costs, premiums would eventually settle at a point about 10 percent lower than they are currently expected to be in 2026.

But the reason why is hardly worth bragging about. As Casey Quinlan notes, Ryan’s bill “gets rid of the requirement for insurers to offer more generous plans,” and it lowers premiums because “insurance would be so expensive for older people that they would exit the market and become uninsured.”

Younger, healthier people would be able to buy cheaper plans in large part because many of the most expensive patients would no longer be able to afford coverage — and thus would no longer draw upon younger people’s premiums to pay for their care. Especially vulnerable patients, meanwhile, would be left in the cold.

A pattern of bad design

The Obamacare replacement disaster isn’t an isolated incident.

Remember Ryan’s Social Security proposal, the one the Bush White House called “irresponsible?” That proposal would have diverted so many tax dollars into private investments that, “by 2050, every single stock or bond in the United States would be owned by a Social Security account.”

As Dylan Matthews explains, “this would mean that the portfolio managers at the Social Security Administration would more or less control the entire means of production in the United States.” In seeking to give private markets a great role in American’s retirement planning, Ryan accidentally came up with a proposal to transform the United States into a communist nation.

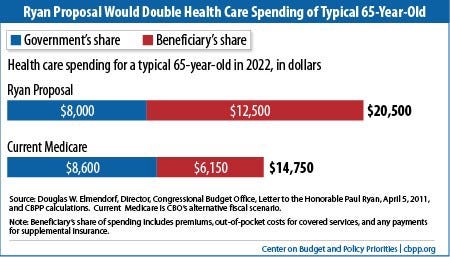

Similarly, Ryan’s 2011 plan to phase out the Medicare program did not simply “end Medicare as we know it,” the weaselly phrase Democrats were forced to adopt after policy-illiterate pundits criticized them for describing Ryan’s plan accurately. Ryan’s proposal would have ended Medicare, period.

Under this 2011 plan, Medicare died in two phases. First, Ryan would have repealed traditional Medicare, the single-payer system most seniors rely on for care, and replaced it with a voucher that offset some of the cost of a private health plan. Because private health insurance has higher administrative costs and typically pays higher prices than a government-run plan, however, this shift to a voucher program would have doubled a typical 65 year-old’s out of pocket expenses.

Phase two began once Ryan’s new vouchercare program was in place. Though the vouchers would gain value in absolute dollars over time, they grew in value less slowly than the rate of health inflation. Thus, with each passing year, Ryan’s vouchers would cover less of an older American’s health premiums. According to CBO, “by 2080, Medicare would be cut 76 percent below its projected size under current policies.” Eventually, the vouchers would become virtually worthless.

When Ryan originally released this proposal, many of his opponents suspected that the vouchers were intentionally designed this way — that is, they were designed to phase out Medicare because Ryan’s wanted to eliminate Medicare. Yet, in 2012, Ryan released a new Medicare proposal that, while keeping the plan to replace traditional Medicare with vouchers, also provided that the vouchers would grow at the rate of health inflation.

It’s possible Ryan made this concession because he realized he couldn’t sell a proposal that would eventually slash Medicare to the point of virtual non-existence. But it is equally likely that he did not understand his original proposal, and had to correct it once real experts in health policy pointed out his error.

The myth of Paul Ryan

There is no one in Washington — possibly no one in America — whose reputation for basic competence outstrips the reality more than Paul Ryan. People with actual policy expertise have been pointing this fact out for years. Yet, somehow, the myth of Ryan as the Great Policy Wonk continues.

Now, here we are, with Ryan facing his first big test as a lawmaker who actually has the real ability to govern — and the speaker could not have blown his trip to the Super Bowl any more spectacularly.

It’s time to put to bed the myth that Paul Ryan has any idea what he’s doing.

***

Reposted from Think Progress.

***

Photo by DonkeyHotey on Flickr.